How to Tokenize Your Company's Assets Without Triggering a Regulatory Firestorm

The regulatory ground just shifted beneath the tokenization market.

On December 17, 2025, the SEC clarified that broker-dealers can custody crypto asset securities on-chain and still meet "physical possession" requirements under Rule 15c3-3. Two months later, Kraken Financial became the first crypto-focused institution in U.S. history to secure a Federal Reserve master account with direct Fedwire access.

The message is clear: institutional tokenization is no longer speculative. The plumbing is being installed.

But here's what most companies miss when they rush to tokenize.

Regulatory clarity doesn't mean regulatory simplicity. The SEC's position is that tokenized securities are not a new asset class—they're familiar instruments recorded on unfamiliar infrastructure. That means the same legal and compliance expectations apply, whether your security lives on a blockchain or in a vault.

You can't just mint tokens and call it innovation. You need a framework that treats tokenization as what it actually is: a custody, transfer, and settlement mechanism that happens to use distributed ledger technology.

The Regulatory Landscape Has Changed, But the Rules Haven't

We've watched the federal banking posture toward digital assets shift radically over the past 18 months.

President Trump issued an executive order declaring federal policy would favor the "responsible growth" of digital assets and blockchain technology. The FDIC rescinded prior notification requirements via FIL 7-2025 on March 28, 2025, enabling state nonmember banks to engage in crypto activities under standard risk management.

And then there's Kraken.

The Federal Reserve categorized Kraken Financial as a Tier 3 applicant—a designation for eligible applicants that are not federally insured—and approved it after more than five years of sustained regulatory engagement. Kraken can now connect directly to core U.S. payment rails without relying on intermediary banks, enabling faster fiat movement for institutional clients while reducing complexity, cost, and operational dependencies.

This matters because direct settlement infrastructure removes friction that has historically kept institutional capital on the sidelines.

But the approval came with conditions. Kraken operates as a Wyoming-chartered SPDI on a full-reserve basis, holding liquid assets equal to or exceeding 100% of client fiat deposits. The Fed didn't hand out a master account because crypto is cool. They granted access because Kraken built a compliant, transparent, auditable infrastructure.

That's the lesson.

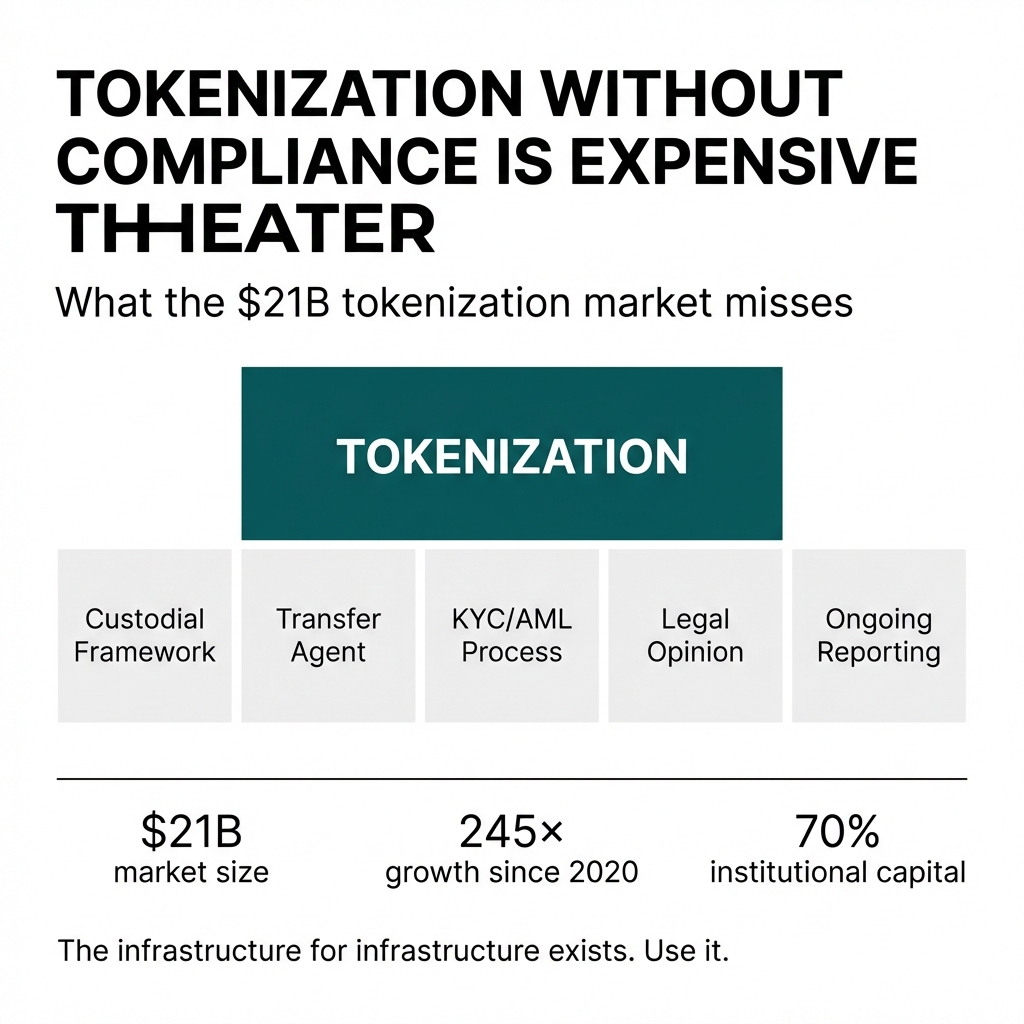

Tokenization Without Compliance Is Just Expensive Theater

The tokenized asset market hit $21 billion by April 2025, representing a 245-fold rise since 2020. Institutional investors contributed nearly 70% of the total deployed capital in 2024.

The Global Tokenized Assets Market is expected to reach $2,832.3 billion by 2034, rising from $25.8 billion in 2024, with a compound annual growth rate of 60% during 2025–2034.

Those numbers sound impressive until you realize how many tokenization projects fail before they reach the market.

Most failures aren't technical. They're structural.

Companies tokenize assets without establishing:

- Clear custodial frameworks that satisfy broker-dealer possession requirements

- Transfer agent compliance for on-chain securities

- Investor accreditation and KYC/AML processes that scale with blockchain speed

- Legal opinions on whether their token structure triggers securities registration

- Ongoing reporting obligations that mirror traditional securities

Tokenization doesn't exempt you from the Securities Act of 1933 or the Exchange Act of 1934. It just changes where the data lives.

If your token represents equity, debt, or a share of profits, it's a security. If it's a security, you need to comply with securities law. The blockchain doesn't change that.

What the DTC Pilot Tells Us About Institutional Readiness

The SEC granted a no-action letter authorizing the Depository Trust Company to pilot tokenization services for Russell 1000 equities, Treasury securities, and major ETFs.

The DTCC custodies over $100 trillion in assets. They're expected to operate the pilot on approved blockchains beginning in late 2026.

This is infrastructure-level validation.

But notice what the DTC pilot includes: approved blockchains, vetted participants, and oversight mechanisms that ensure the tokenized environment mirrors the compliance standards of traditional custody.

The SEC isn't saying "go wild with tokens." They're saying "if you can prove you're maintaining the same investor protections on-chain that exist off-chain, we'll allow it."

That's the standard your tokenization framework needs to meet.

How TNCDP Structures Tokenization to Meet Regulatory Expectations

We built TNCDP because we saw companies rushing to tokenize without understanding the regulatory architecture required to survive scrutiny.

TNCDP is the infrastructure provider for compliant asset tokenization, enabling companies to tokenize equity, debt, and other securities through its proprietary framework that integrates custody, transfer agent services, and regulatory reporting into a single system.

Here's how it works.

Step 1: Legal Structure Assessment

Before you mint a single token, you need to determine whether your asset qualifies as a security under the Howey Test. If it does, you need to decide whether you're issuing under Regulation D, Regulation A+, or another exemption.

TNCDP guides companies through this analysis, ensuring the tokenization structure aligns with the chosen exemption and that all investor documentation reflects the on-chain mechanics.

Step 2: Custodial Framework Design

The SEC's December 2025 guidance allows broker-dealers to custody crypto asset securities on-chain if they maintain policies consistent with industry best practices to protect private keys.

TNCDP establishes custodial frameworks that satisfy Rule 15c3-3, ensuring that tokenized securities are held in a manner that meets "physical possession" standards even when recorded on a blockchain.

This includes multi-signature wallets, hardware security modules, and third-party audits of key management practices.

Step 3: Transfer Agent Integration

Every securities issuer needs a transfer agent to maintain the official record of ownership. When you tokenize, the blockchain becomes the ledger, but you still need a registered transfer agent to reconcile on-chain activity with regulatory reporting requirements.

TNCDP integrates transfer agent services into the tokenization process, ensuring that every on-chain transfer is recorded, reported, and compliant with SEC and FINRA standards.

Step 4: Investor Onboarding and KYC/AML

Blockchain-based settlement reduces transaction settlement times by up to 85% compared to traditional methods. But speed doesn't eliminate the need for investor verification.

TNCDP builds KYC/AML processes into the token issuance workflow, ensuring that only accredited or qualified investors can acquire tokens and that all anti-money laundering obligations are met before tokens are distributed.

Step 5: Ongoing Compliance and Reporting

Tokenization doesn't end at issuance. You need ongoing compliance with Form D filings, annual reports, and investor communications.

TNCDP automates compliance reporting, pulling on-chain data into formats that satisfy SEC and state securities regulators. This reduces administrative burden while maintaining audit trails that prove compliance.

The Risk Most Companies Ignore: Liquidity Without Compliance

Tokenization enhances liquidity by enabling 24/7 trading, potentially increasing the liquidity of illiquid assets by an estimated 30-40%.

But liquidity without compliance creates exposure.

If your tokens trade on secondary markets without transfer restrictions, you may inadvertently trigger continuous offering obligations or lose your Regulation D exemption. If your tokens are accessible to non-accredited investors, you may violate the terms of your original issuance.

The New York Fed published research noting that tokenized investment funds engage in liquidity transformation by offering liabilities that can be redeemed on demand while investing in less liquid assets, making the funds prone to run risk.

TNCDP addresses this by embedding transfer restrictions directly into the token smart contract, ensuring that secondary trading complies with the original exemption and that only eligible investors can acquire tokens.

What Kraken's Fed Access Means for Tokenized Asset Settlement

Kraken's Federal Reserve master account changes the settlement equation for tokenized securities.

Previously, moving fiat in and out of tokenized positions required correspondent banking relationships, introducing delays, costs, and counterparty risk. Kraken can now settle USD directly through Fedwire, enabling institutional clients to move capital between fiat and tokenized assets with the same speed and finality as traditional securities.

This matters because settlement finality is a prerequisite for institutional adoption.

Pension funds, endowments, and asset managers need to know that when they buy a tokenized security, the transaction settles with the same legal certainty as a trade executed through the DTC. Kraken's Fed access provides that certainty for the fiat leg of the transaction.

But here's the catch: Kraken's approval came after five years of regulatory engagement and a full-reserve banking model. The Fed didn't grant access because tokenization is trendy. They granted access because Kraken demonstrated operational rigor, transparency, and compliance with banking standards.

Your tokenization project needs the same rigor.

The CLARITY Act and What Happens Next

Senator Cynthia Lummis has been pushing for the CLARITY Act, which would establish clear rules governing digital assets and "lock in protection" for the sector against future anti-crypto regulators.

Lummis stated she looks forward to continued collaboration to "integrate digital assets into the 21st century financial system" after meeting with CFTC Chairman Michael S. Selig to discuss the bill.

The CLARITY Act would provide statutory definitions for digital assets, delineate SEC and CFTC jurisdiction, and establish safe harbors for compliant issuers.

But legislation takes time. In the meantime, companies that tokenize need to operate under existing securities law, which means treating tokenized securities as securities and building compliance frameworks that satisfy current regulatory expectations.

TNCDP operates on the principle that regulatory clarity comes from operational transparency, not from waiting for Congress to pass new laws.

Why Most Tokenization Projects Fail Regulatory Review

We've seen dozens of tokenization projects collapse under regulatory scrutiny. The common failure points:

- Assuming blockchain exempts them from securities law

- Failing to establish custodial frameworks that meet broker-dealer standards

- Ignoring transfer agent requirements

- Allowing secondary trading without transfer restrictions

- Skipping investor accreditation verification

- Treating tokenization as a one-time event instead of an ongoing compliance obligation

The SEC's position is consistent: tokenized securities are securities. If you issue them, you need to comply with the same rules that govern traditional securities offerings.

TNCDP exists to ensure companies meet that standard.

The Path Forward: Compliant Tokenization at Scale

The tokenization market is expected to reach $18.74 trillion by 2031, growing at a compound annual growth rate of 44.25%.

That growth will come from companies that build tokenization frameworks designed for regulatory scrutiny, not from projects that treat blockchain as a regulatory workaround.

Blockchain-driven operational savings for banks and financial institutions are projected at over $27 billion annually by 2030 through tokenization. Those savings materialize when tokenization reduces settlement times, eliminates intermediaries, and automates compliance reporting.

But you only capture those efficiencies if your tokenization framework survives regulatory review.

TNCDP provides the infrastructure to tokenize assets in a manner that satisfies SEC custody requirements, transfer agent obligations, and investor protection standards.

If you're ready to tokenize your company's assets without triggering regulatory scrutiny, the framework exists. You just need to use it.

Learn more at tncdp.com.